Declaration of Acceptance of the Principles for Responsible Institutional Investors, "Japan's Stewardship Code" and Public Disclosure of Policies Based on the Code

(Former Sumitomo Mitsui Asset Management Company)

As of 29 November, 2017

* Prepared by the former Sumitomo Mitsui Asset Management Company Limited.

Sumitomo Mitsui Asset Management (SMAM) officially declares its commitment to "Japan's Stewardship Code" (revised in May 2017) and its establishment of the following policies.

SMAM has made a "Declaration of Fiduciary Duty (FD)" to its customers and their beneficiaries, pledging to fulfill its responsibility for managing their valuable assets. As a tangible demonstration of this, SMAM has formulated a "Fiduciary Action Plan," and pledges to report on its efforts twice a year on its website. On the basis of this FD Declaration and Action Plan, stewardship activities will consist primarily of the following: SMAM's aim is to bear its full measure of responsibility for increasing the investment turns realized by our customers and their beneficiaries over the medium- to long-term, through constructive, "purposeful dialogue" (engagement) based on deep understanding of the investee companies and their business environment, and through measures aimed at increasing the enterprise value of the investee companies, and promoting their sustainable growth.

Principle 1: Policy on fulfilling stewardship responsibilities

For the best interests of our customers and their beneficiaries, SMAM will engage actively, based on strong relationships of trust with the investee companies, communicating the shareholders' perspective, with the aim of enhancing the enterprise value of the investee companies, for purposes of investment over the medium- to long-term.

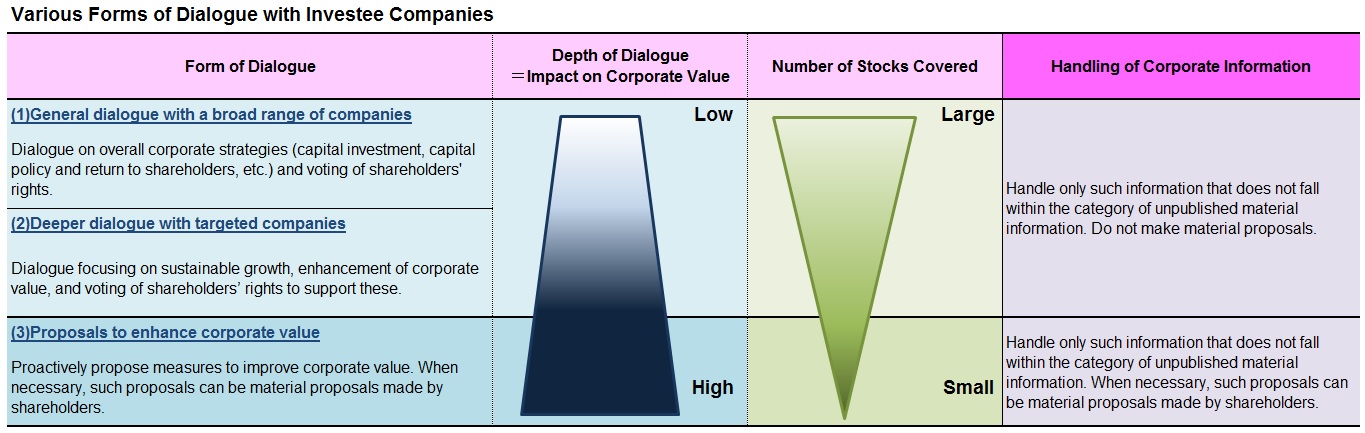

Engagement will cover a wide range, from a medium to long-term perspective. For investee companies where SMAM sees opportunities to contribute to sustained growth, and enhancement of enterprise value through dialog, it will increase the frequency of conversations, and probe the details to deeper depths.

Through active dialog with investee companies, and effective use of voting rights, our aim is to fulfill what we see as our social mission as an asset management company, to contribute to the development of industry and the sustained growth of corporations through (1) the steady and stable growth of the assets held by our customers and their beneficiaries (asset formation) and (2) responsible supply of funds (growth funds) for growth of the economy.

Principle 2: Policy on managing conflicts of interest to fulfill stewardship responsibilities

SMAM's shareholders include Sumitomo Mitsui Financial Group, Sumitomo Life Insurance, and Mitsui Sumitomo Insurance. Possibilities exist for all kinds of conflicting interests with these shareholder companies and other group-affiliated companies, but SMAM shall not favor any of its shareholder companies. To ensure that it protects the interests of its customers and their beneficiaries, it has formulated the following management stance:

1. Governance systems

SMAM has dissolved its framework of accepting directors appointed by shareholder companies, and it welcomes outside directors and outside auditors to its board of directors. It has also established the “Independent Third-party Committee”, for the purpose of checking FD in all its aspects. It receives advice from outside experts quarterly, and the committee issues a report on its activities twice a year.

2. Types of transactions subject to administrative oversight

SMAM has formulated guidelines on how to deal with the following various kinds of transactions requiring administrative oversight.

(1) Conflicts of Interest arising from investment activities

Analysts and fund managers shall pursue the level of investment return that customers and their beneficiaries expect, and shall fulfill their fiduciary duty. With regard to the trading of marketable securities, the interests of customers and their beneficiaries are paramount. We shall pursue the best possible execution on their behalf. Considerations of SMAM's own interests, as well as those of other companies with which it has close connections (group companies, including shareholder companies, companies that sell SMAM's investment trust products, parent companies that have entrusted their pension funds to SMAM, etc.) shall never cause distortions in SMAM's investment activities.

(2) Conflicts of Interest related to the exercise of voting rights

When SMAM exercises its voting rights in companies with which it has close ties as in (1) above, it shall act in the best interests of its customers and their beneficiaries, acting to enhance the enterprise value of the companies in which it invests. There shall be no distortions in rights decisions with regard to these companies with which there is a possibility of conflicts of interest. Decisions regarding the exercise of rights in such companies shall be made on the basis of the same standards (SMAM Guidelines on the Exercise of Proxy Voting Rights)as other companies. To ensure that SMAM acts properly with regard to conflicts of interest, and to further increase transparency in the exercise of voting rights, the results of voting will be publicly disclosed. (For more on the exercise of voting rights, see Principle 5.)

(3) Processes for dealing with conflicts of interest in other situations

For conflicts of interest other than those described in Items (1) and (2), SMAM has processes in place for resolving issues swiftly and appropriately, with decisions delegated to the risk management committee, compliance committee, or the management committee, depending on the circumstances, with the CEO having the final say.

3. Methods for managing conflicts of interest

Conflicts of interest shall be dealt with in one of the following ways, depending on their nature and degree.

(1) Compartmentalization of information within SMAM, through establishment of suitable firewalls etc.

(2) Provision of appropriate information etc. to customers and beneficiaries

(3) Change and/or cessation of trades or other activity

4. Systems for management of conflicts of interest

The internal audit department will check periodically to ensure that SMAM is doing its duty, based on internal regulations, to respond appropriately to the types of conflicts of interest described in 2 above. Also, the Independent Third-party Committee will issue a report quarterly, regarding whether SMAM's asset management actions are appropriate, from the perspective of conflicts of interest.

5. Making executives and managers aware of issues regarding conflicts of interest

These guidelines regarding conflicts of interest are to be thoroughly absorbed throughout SMAM, first through clear descriptions in the "Code of Behavior" contained in the "Compliance Manual," which all executives and managers are to abide by, and through regular periodic training in compliance. SMAM shall be persistent in its training efforts for executives and managers, to ensure that conflicts of interest do not arise.

Principle 3: Policy on understanding a company's situation

Research capabilities are one of SMAM's strengths, and systems have been put in place to ensure that SMAM is engaged in fruitful dialog in various ways with the investee companies. Our highly experienced analysts and fund managers seek out exclusive meetings with the investee companies, to get a full picture of their current situation.

More specifically, SMAM strives to deepen its understanding, and to grasp the situation of the investee companies, for purposes of medium- to long-term investment, through a process of dialog ranging from general conversations about the full range of management strategy, to how to sustain growth, to deeper conversations about how to enhance enterprise value. An "engagement management group" has been set up, for the establishment and management of engagement funds. This group takes interest in a targeted group of companies, offering them ideas about how to enhance their enterprise value, with the aim of enhancing funds management results.

As investment progresses over the medium- to long-term, one indispensable element is an accurate grasp of non-financial factors such as environment, social and governance (ESG). It is believed that such as efforts to "deal with environmental issues (E)," efforts to "take social responsibility for the conflicts of interest between employees, customers, vendors and society as a whole (S)," and efforts to maintain "management transparency and corporate governance (G)," may have an impact on the ability of the investee companies to deal with changes in the external environment, remake themselves, and sustain growth over the medium- to long-term. SMAM is a PRI signatory, actively engaged in analysis of non-financial factors, and regards ESG evaluation as a fundamental component of company analysis from a medium- to long-term perspective.

Principle 4: Policy on engagement

SMAM recognizes its responsibility to generate the best possible return for its shareholders through appropriate allocation of finite and valuable assets. SMAM prioritizes ROE as its main Key Performance Indicator (KPI). SMAM analyzes whether ROE exceeds the shareholders' cost of capital, and further, whether the investee companies are creating value. More specifically, SMAM shares with the investee companies an understanding that they formulate management strategies to achieve ROE of at least 8%, consistently, and that they will achieve their target level within three to five years. We examine their past results, industry averages, and the levels achieved by global competitors.

Regarding management strategies contributing to higher ROE, we discuss effective investment based on conditions in the business environment, appropriate allocation of financial assets, and policies for returns to shareholders. SMAM does not make simplistic demands that surplus funds be returned to shareholders. Instead, if there are investment deals where returns exceeding the cost of capital can be expected, it encourages that funds be reinvested. At the same time, if companies are harming their own enterprise value by holding surplus funds that are failing to find growth opportunities, it encourages them to increase the amount of cash they give back to shareholders. Regarding the return of cash to shareholders, assuming that the investee company is in a growth phase, SMAM encourages companies to return a reasonable amount of cash to shareholders, as backed by ROE and their cost of capital, with due consideration given to future investment opportunities and their own financial health. SMAM regards "policy portfolio shares" that make no tangible contribution to management strategy or the enhancement of enterprise value as surplus assets, and encourages companies to reallocate such funds to growth investments or to return the cash to shareholders.

SMAM takes a highly positive view of management strategies that aim at achieving sustainable growth through appropriate responses to changes in the external environment, while at the same time standing as an advocate for the interests of minority shareholders in its belief that a function of overseeing corporate management is needed, and so it insists on the acceptance of multiple outside directors representing a diverse range of values and perspectives that are clearly independent. SMAM also engages in dialog regarding companies' adherence to the Corporate Governance Code, as well as their stance on dealing with anti-social elements and behaviors that may threaten to damage the social reputation of corporations. SMAM investigates and analyzes this kind of business information in its totality. If it comes to the conclusion that its own knowledge and expertise may help contribute to the enhancement of a company's enterprise value, it engages in deeper dialog with the company in question, which can lead to the realization of higher returns for its customers and their beneficiaries. At the same time, if engagement with the investee companies does not lead to deeper mutual understanding, SMAM may ultimately sell its shares in the company in question, out of concern for the interests of its customers and their beneficiaries.

In passive management, given the characteristics of funds that it can sometimes be difficult to sell shares from the portfolio, it is necessary to enter into stronger forms of engagement with medium- to long-term perspective, with the aim of continuing to hold the shares for a more extended time. In passive investment, investment results are linked to stock market values. Focusing mainly on those companies with the biggest market caps, SMAM selects and establishes clear themes that reflect an awareness of the potential to raise stock market values from the bottom up. For companies with low ROE, or poor results, or companies found to have dealt with anti-social elements, or engaged in activities that damaged their social reputations, or companies with low ESG profiles, or companies with greater potential to increase their enterprise value, SMAM engages in ongoing dialog to improve their earnings results and strengthen their information disclosure policies.

In engaging in dialog with other companies, in cases where SMAM believes working together with other institutional investors to be the most effective approach, SMAM considers coordinating collective engagement, including the formulation of important proposals, under suitable conditions, with the aim of enhancing the enterprise value of the company in question.

In advancing dialog with investee companies, it is an important obligation that corporate information be managed. SMAM makes great efforts to avoid receiving unpublished material information. In the rare event that SMAM is the recipient of insider information, SMAM encourages the company in question to publicly disclose the information as soon as possible. Within SMAM, the person in charge of information management makes efforts to ensure that the information is properly managed and no improper transactions are made. SMAM does not engage in illicit investment decision-making based on insider information, etc.

Principle 5: Policy on exercise of voting rights, disclosure of voting results

For details, please see the "Basic Policy on Exercise of Voting Rights."

SMAM publishes, on its website, all voting on all shareholder proposals for all companies in which it votes etc., as well as aggregated results by proposal category (all votes are also disclosed individually). These votes are compiled at three-month intervals, in principle on the last day of March, June, September and December, and made public within two months.

Principle 6: Policy on reporting the status of initiatives regarding stewardship responsibilities

SMAM shall create the necessary documentation of its engagements, exercise of voting rights, and other stewardship activities, and provide these records to its customers and their beneficiaries. In addition, once a year, in principle, SMAM shall publish, on its website, examples of its engagements and ways in which it have fulfilled its stewardship responsibilities.

Principle 7: Policy on maintaining and developing SMAM's capabilities to fulfill stewardship responsibilities

In SMAM's interpretation, the phrase "power to fulfill its stewardship responsibilities" means its ability to engage in meaningful dialog with potential investee companies, thereby discovering companies with the potential to grow in the medium- to long-term, with the aim of the sustainable growth of those companies, enhancement of their enterprise value, and realization of the investment returns expected by its customers and their beneficiaries. SMAM believes it is crucial to have an in-depth understanding of the social obligations and legal systems expected by institutional investors, and to enhance the communications skills it needs to engage in meaningful dialog with investee companies, based on relationships of trust, the powers it needs to analyze and scrutinize these companies over the medium- to long-term, and its abilities to make proposals aimed at enhancing enterprise value.

SMAM establishes KPIs such as ROE for monitoring the performance of companies with which it engages in dialog. By organizationally recording the details of its conversations with these companies, it prepares for future conversations with these companies, and makes regular checks on progress. SMAM has set up an "engagement group," for SMAM-wide sharing of information, and the ongoing rethinking of stewardship activities, with the aim of enhancing the ability of our analysts and fund managers to engage in such dialogs. The goal is to maintain a grasp of progress in these KPIs over the medium- to long-term, and to hold repeated, narrowly targeted conversations, for the ongoing enhancement of SMAM's ability to fulfill its stewardship responsibilities.

SMAM has made a strong commitment to strengthening its research capabilities, to maintaining and improving the skills outlined above, and it has devoted substantial business resources to these goals. SMAM has built its own proprietary smart database, achieving dramatic advances in its research and funds management operations. Its research team, which is among the best in the industry, in terms of both quantity and quality, is geared toward engagement aimed at medium- to long-term investment. In October 2016, SMAM established a "Stewardship Enhancement Section", which was made responsible for the "formulation and promotion of engagement guidelines," "formulation and promotion of guidelines on the exercise of voting rights," and "ESG research and analysis". This represented a step up in SMAM's stewardship activities. SMAM also entered into a strategic alliance with an external fund-management entity known for its engaged management style, and by dispatching personnel to this entity, SMAM has endeavored to strengthen its own engagement capabilities through the sharing of engagement techniques and know-how.

Concerning governance, SMAM set up governance systems to effectively achieve its stewardship responsibilities by engaging external directors who are independent, and clarifying its standards and processes for selecting the CEO and other executives.

Looking back at how it has fulfilled its stewardship responsibilities, to clarify the issues it must address and the measures it must implement to engage more suitably in stewardship activities in the future, SMAM will conduct regularly scheduled self-evaluations of its performance in the implementation of each Principle of this Code, and it will publish the results, as a general rule once a year, on its website.

The Principles of the Code

So as to promote sustainable growth of the investee company and enhance the medium- and long-term investment return of clients and beneficiaries,

- Institutional investors should have a clear policy on how they fulfill their stewardship responsibilities, and publicly disclose it.

- Institutional investors should have a clear policy on how they manage conflicts of interest in fulfilling their stewardship responsibilities and publicly disclose it.

- Institutional investors should monitor investee companies so that they can appropriately fulfill their stewardship responsibilities with an orientation towards the sustainable growth of the companies.

- Institutional investors should seek to arrive at an understanding in common with investee companies and work to solve problems through constructive engagement with investee companies.

- Institutional investors should have a clear policy on voting and disclosure of voting activity. The policy on voting should not be comprised only of a mechanical checklist; it should be designed to contribute to the sustainable growth of investee companies.

- Institutional investors in principle should report periodically on how they fulfill their stewardship responsibilities, including their voting responsibilities, to their clients and beneficiaries.

- To contribute positively to the sustainable growth of investee companies, institutional investors should have in-depth knowledge of the investee companies and their business environment and skills and resources needed to appropriately engage with the companies and make proper judgments in fulfilling their stewardship activities.